Content:

Nature of Accounts and Rules of Debit and Credit

Classification of Accounts, rules of debit and credit

Preparation of accounting vouchers and supporting documents

(Bills, Cash Memo, Debit Note, Credit note)

Learning Outcomes:

Understanding the Classification of accounts

Explaining the rules of debit and credit

Application of the rules of debit and credit

Preparation of accounting vouchers with the help of supporting documents

What is an Account?

An Account, abbreviated as A/C, is a record of business transaction. The simplest form of an Account looks like the English letter ‘T’. It is divided into two parts – the left side of the ‘T’ is Debit (abbreviated as Dr.) and the right side is Credit (abbreviated as Cr.). When recording each transaction, the total amount debited must be equal to total amount credited. In accounting format – debit and credit indicate whether the transactions are to be recorded on the left-hand side or right hand side of the account.

See the Illustration below:

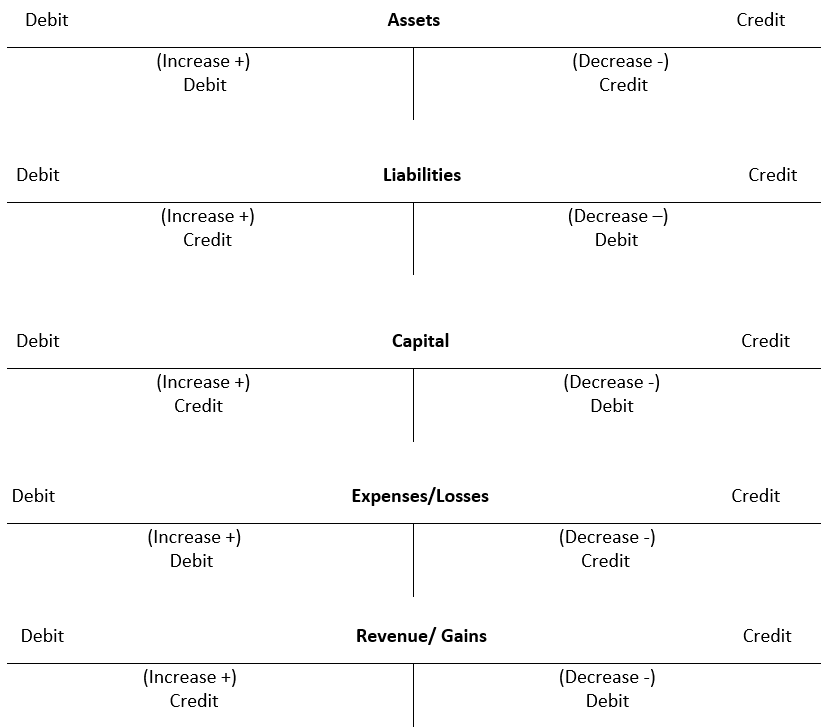

Modern Classification of Accounts:

All accounts are divided into five categories for the purposes of recording the transactions:

a) Asset

b) Liability

C) Capital

D) Expenses/ Losses

E) Revenues/Gains

Rules of debit and credit:

Two fundamental rules are applied in respect of the accounts mentioned above to record the changes.

1. For recording changes in Assets, Expenses/Losses:

i) Increase in asset is debited and decrease in asset is credited

ii) Increase in expenses/losses is debited and decrease in expenses/losses is credited

2. For recording changes in Liabilities, Capital, Revenues/Gains:

i) Increase in liabilities credited and decrease in liabilities debited

ii) Increase in capital is credited and decrease in capital is debited

iii) Increase in revenue /gain is credited and decrease in revenue /gain is debited

The above rules can be summarised in “T” account format as follows:

Application of the Rules of Debit and Credit

Transaction 1.

Mohit started business with cash ₹20000

Analysis of the transaction:

The transaction increases cash in one hand and increases capital on the other. As per rules increase in asset (cash+ is debited and increase in capital is credited. The transaction will be recorded as follows:

Transaction 2.

Mohit purchased goods for cash ₹5000

Analysis of the transaction:

Purchase is an expense and increase in expense is debited

Cash is an asset, decrease of asset is credited

So, the transaction will be recorded as follows:

Transaction 3.

Sold goods for cash ₹8000

Analysis of the transaction:

Sales is a revenue account, increase in revenue will be credited

Cash is an asset, increase of asset will be debited

Therefore the transaction will be recorded as – debit cash account and credit sales account.

Transaction 4

Paid electricity bill ₹1000

Analysis of the transaction:

Electricity is an expense which decreases capital and is thus recorded in debit side

Cash paid for electricity reduces asset and should be credited.

Transaction 5

Purchased office furniture ₹4000 and issued a cheque

Analysis of the transaction:

Here we see an increase in the value of assets which in this case is furniture. It should therefore be debited.

A cheque has been issued as payment which would reduce Bank balance thus decreasing asset. So, Bank account should be credited.

6. Transaction:

Paid wages ₹3000

Analysis of transaction:

Wages is an expense and increase in expense has to be debited. Cash is an asset which will decrease for paying wages so, cash a/c will be credited.

7. Transaction

Received interest ₹1000

Analysis of transaction:

Receiving interest is gain and any addition of gain is credited as it adds up to capital. Interest is received in the form of cash which is an asset. Addition to asset is debited.

8. Transaction:

Sold goods to Rajat ₹5000

Analysis of transaction:

Sale of goods is Revenue A/C, any increase in revenue is credited. Sales account will be credited. The transaction increases debtor which is an asset and Rajat as debtor has to be debited.

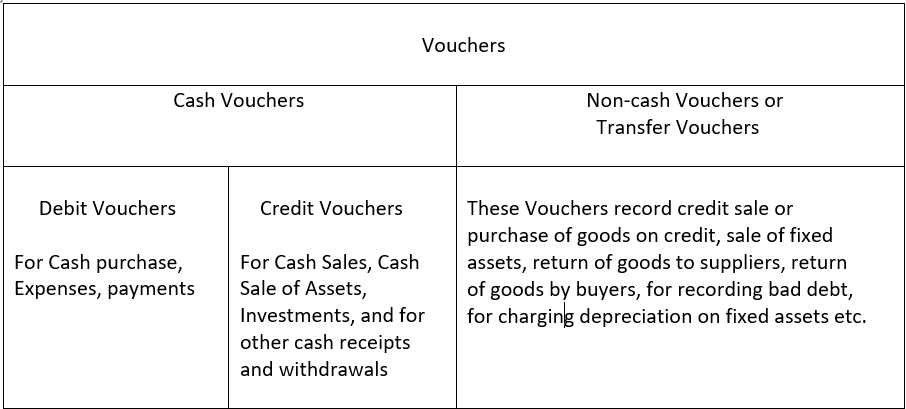

Accounting Vouchers:

Accounting vouchers are the basis of accounting entries. Business transactions are evidenced by appropriate documents such as cash memo, invoice, sales bill, pay-in-slip, salary slip etc. Vouchers are prepared from these source documents and arranged in chronological order. They are then recorded in the books of original entry (journal). Without accounting vouchers no worthwhile accounting process can be undertaken.

Accounting Vouchers may be classified as below:

Supporting (or Source) documents:

Business transactions are usually evidenced by appropriate documents such as Cash Memo, Invoice, Sales Bill, Pay-in-slip, cheques, salary slip etc. These are proofs of transactions for which accounting entries will have to be passed. The functions of source documents are as follows:

1. Transaction evidence: The first and the most important step in recording transactions as per accounting rules is to establish documentary evidence of the transactions. The transactions are first identified on the basis of source documents and then recorded in the books of account. Every transaction has to be supported by a document.

2. Basis of vouchers: Source documents or Supporting documents are the basis of preparing accounting vouchers

3. Authorisation: These documents are signed by an authorised person

4. Audit support: These documents play a key role in auditing of accounts as they are presented as documentary evidence of transactions.

Types of Source Documents:

1. Cash Memo: The Cash memos are for cash sale or purchase. Here, one gets the date of purchase, description of goods but may not include name of the buyer as it is a cash transaction. However, it must mention the seller’s name along with GST no.

2. Invoice or Bill: An Invoice or Bill is generated when a seller sells goods on credit. Unlike the cash memo, the Invoice or Bill contains name of the buyer along with GST no. It must also must contain the Bill / Invoice no. date, order no. detail of goods and seller’s details.

3. Receipt: Money receipts are recognition of any transaction involving cash. It is a vital source document for accountants.

4. Pay-in-slip: When cash or cheque is deposited in a Bank it is done through a printed document called pay-in-slip supplied by the bank. Here details of cash or cheque amount, denominations, cheque number etc are written and the counterfoil is signed by the Bank as a receipt.

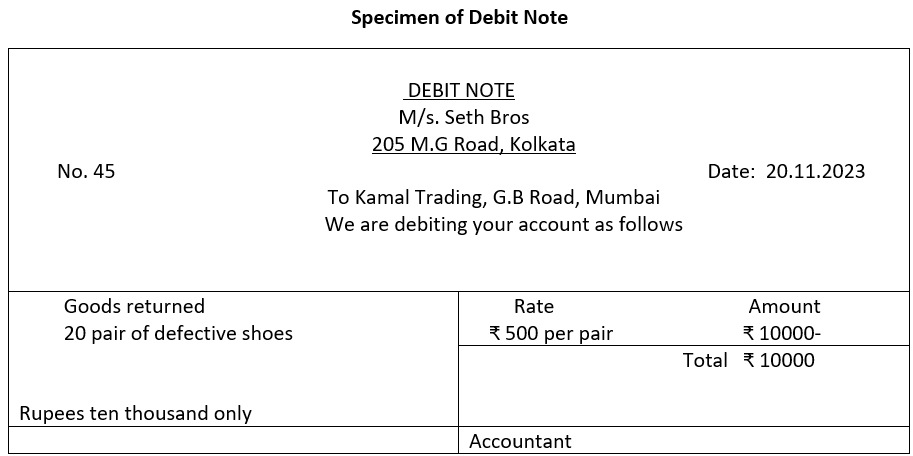

5. Debit note: This is a document sent by a buyer to a seller when a part of the goods is not up to the mark, and the buyer chooses to return them. A note is prepared to debit the supplier account. It is called a Debit Note and is raised to reduce the amount payable to the seller. A Debit Note is made in duplicate, the original copy is sent to the supplier and the duplicate copy is retained for future reference.

Illustrative Transaction: M/s. Seth Bros returns goods worth ₹10000 to M/s. Kamal Trading for poor quality.

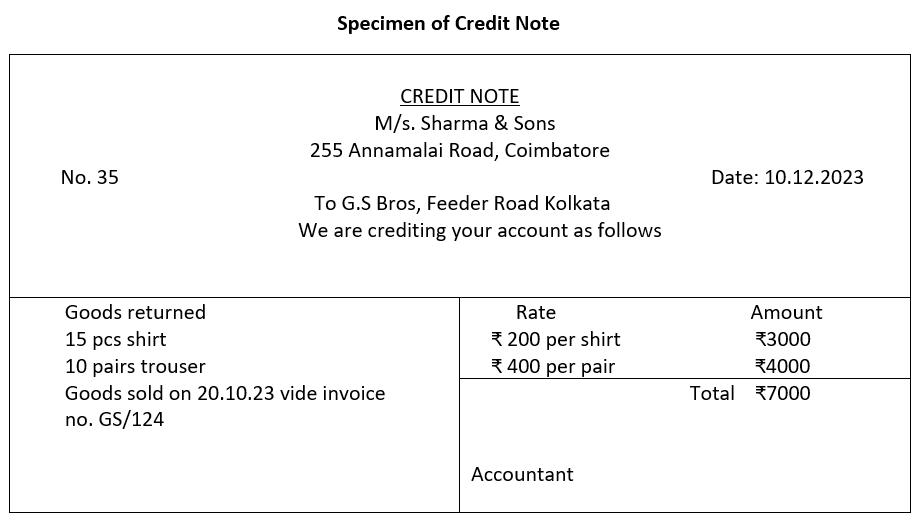

6. Credit Note: This document is issued by a seller to a buyer as an acknowledgement of goods returned by the buyer. A Credit Note is issued to credit a buyer’s account to transfer money for goods returned. Transaction: M/S. G.S Bros. returns goods worth ₹7000 to M/s. Sharma & Sons for poor quality.

Source documents and Accounting Vouchers – difference

| Source documents | Vouchers | |

| 1. | These documents are basis for writing vouchers | Vouchers are the basis for accounting entries. |

| 2. | Source documents describe transactions | Vouchers determine the debit and credit of the transactions |

| 3. | Source documents are evidence of transactions | Vouchers work upon the evidence and unlike the source documents they are numbered serially. |

Preparing Accounting Vouchers from source documents:

Transaction 1 M/s Patel Bros. sells a 14-inch laptop to M/s Teknocraft for ₹ 30000

Source document: Invoice no.203

Example of Credit voucher (for cash sale)- in the books of Patel Bros.

Transaction 2: Amco Engineering purchases a drill machine from Modern Machinery Corp.

for 10000.

The Source document: Bill/Invoice no.250 issued by Modern Machinery

Debit voucher in the books of Amco Engineering

Transaction 3

Specimen of Credit Voucher (for cash sale)

Transaction: Modern Leather Works sold 10 leather bags to Trends & Co. for ₹ 4000

Source document: money receipt

Credit Voucher in the books of Modern Leather Works

Note: Cash account in cash book will be debited with ₹ 4000.

Transaction 4:

M/S. ABC and Co. paid wages ₹10000

Source Document: Pay Slip

Transfer Vouchers (non-cash vouchers): These vouchers are prepared to record Credit Purchase, Credit Sale, goods returned to party, goods returned by party, sale of old machinery etc.

Transaction 1:

M/s. Newgen Bros. bought 200 ball bearings from SKF industries for ₹20000 on credit

Source document: Invoice no. 556 dt. 8.1.24 issued by SKF Industries

Transaction 2

Returned 20 ball bearings to SKF industries valued at ₹ 2000 dt.20.1.24

CBSE Class 9 Elements of Book-Keeping and Accountancy Unit 3: Nature of Accounts and Rules of Debit and Credit – Completed

We have completed the following topics in this unit:

Content:

Nature of Accounts and Rules of Debit and Credit

Classification of Accounts, rules of debit and credit

Preparation of accounting vouchers and supporting documents

(Bills, Cash Memo, Debit Note, Credit note)

Learning Outcomes:

Understanding the Classification of accounts

Explaining the rules of debit and credit

Application of the rules of debit and credit

Preparation of accounting vouchers with the help of supporting documents