Content:

Need for journal and journal entries

Subsidiary Books – Cash Book, Purchase Book, Sales book, Purchase Return Book, Sales Return Book

and Journal Proper

Learning Outcomes:

Understanding the need for journal

Developing the skill of recording of transactions in journal

Explaining the importance of preparing subsidiary books

The book in which business transactions are recorded for the first time is called Journal. This is why Journal is also called the book of original entry. The word “journal” has been derived from the French word “jour” meaning day. So, journal is the daily record of transactions. The process of recording transactions in journal is called journalising. Journal entries are recorded systematically in a chronological order. The format of a journal is shown below:

The first column on the left is where the transaction date is written. Next is particulars column where the account to be debited is written on the first line with word “Dr.”. The Account title to be credited is written on the second line with a prefix “To”. Below the Account titles a brief description of the transaction called “narration” is given. The Ledger Folio or L.F column mentions the page number of the ledger book where the relevant account appears.

It is to be noted that this column is filled up at the time of posting and not at the time of making the journal entry.

The Need for Journal:

1. Processing primary data: As the book of original entry, the journal classifies transactions for the first time paving the way for books of final entry. The need for journal arises from the fact that it helps streamline the accounting process.

2. Application of Double Entry: Applying the rules of double entry to split a transaction into debit and credit is pivotal for the later accounting process.

3. Past reference: Processing transactions in chronological order helps keep a permanent record of all transactions making quick reference easier in future.

4. Narration: The narration written at the end of each journal entry helps analyse exact nature of the transaction which has been journalised.

Advantages of Journal:

1. Source of primary data: Journal acts as the data bank of transactions with accounting vouchers as source material. This facilitates transaction reference in future.

2. Chronological records: Journal entries are made in chronological order making retrieval of data easy.

3. Subdivision of journal for efficiency: The subdivision of journal into sales book, purchase book etc means work can be distributed among accounts assistants for maximum efficiency.

4. Legal evidence: In case of legal disputes, the relevant papers like bills, vouchers and accounting records can be produced as evidence in the court of law or for arbitration.

5. Narration of transaction: After a journal entry is passed, a narration which is a description of the transaction is written. So, ledger accounts are kept clutter free.

6. Ensuring Double Entry: In journal, every transaction is analysed and recorded as per rules of double entry system. This ensures correct ledger posting later on.

Classification of Accounts and Journalising rules:

| Account Type | Debit | Credit |

| Asset | Increase | Decrease |

| Liability | Decrease | Increase |

| Capital | Decrease | Increase |

| Expenses/ Losses | Increase | Decrease |

| Revenues/ gains | Decrease | Increase |

Examples of Journal Entries:

Example 1:

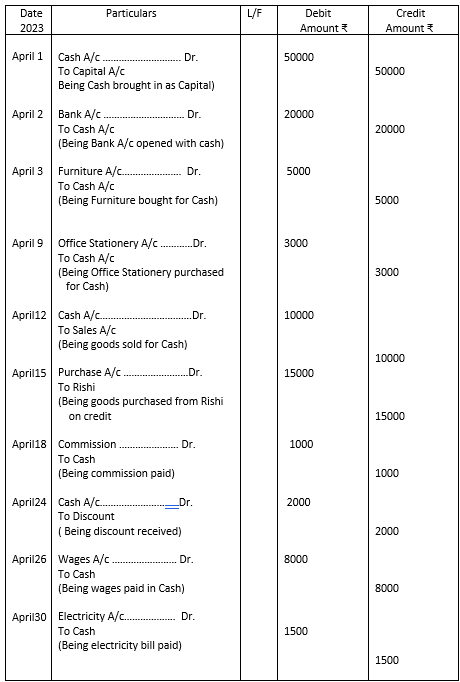

Transaction: Mohan Garg started a business with cash ₹ 50000

Analysis:

i) Cash is Asset, Cash is being added by Mohan Garg – debit cash A/c

ii) Capital – Cash invested by Mohan as capital is liability of the business. Any addition to it is to be credited to Capital A/c.

Example 2:

Transaction: Purchased goods for cash ₹ 10000

Analysis: Purchase is an expense account. Expenses are debited so we debit Purchase A/c

Cash is Asset Account which is getting decreased so, credit Cash A/c

Journal Entry:

Example 3:

Transaction: Purchased furniture from Suven on credit for ₹ 5000

Analysis: Furniture is an Asset account. Here, asset is added to business – debit Furniture A/c

Suven is a Liability account as he is a creditor and liability added is credit balance.

Journal Entry:

Example 4: Transaction: Sold goods for cash ₹ 5000

Analysis: Cash is an Asset A/c, increase in cash asset is to be debited

Sales is a Revenue account, increase in revenue means – Sales A/c to be credited

Journal Entry:

Example 5:

Transaction: Paid Rent ₹ 1000

Analysis: Rent is an Expense Account so, Debit Rent A/c

Cash is an Asset Account. Rent will reduce Cash/Asset so, Cash A/C will be credited

Journal Entry:

Example 6.

Transaction: Paid Electricity Charges ₹ 1000

Analysis: Electricity Charge is an Expense A/C – We have to debit Electricity for additional charges

Cash is an Asset A/c – reduction of cash for payment means Cash A/c is to be credited.

Journal Entry:

Example 7.

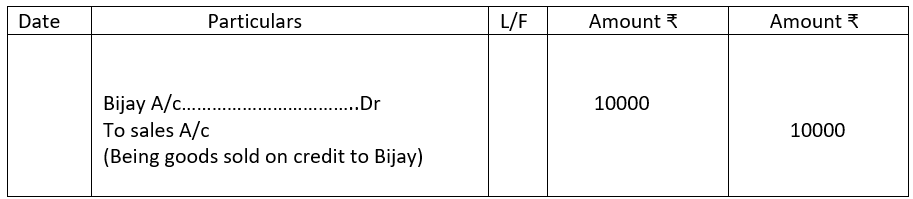

Transaction: Sold goods to Bijay on credit ₹ 10000

Analysis: Bijay is an Asset A/c as he is a debtor owing money to Mohan Garg. When asset value increases the account is debited.

Sales is a Revenue A/c. As it is a gain, we credit Sales A/c

Journal Entry:

Example 8:

Transaction: Goods returned by Bijay ₹ 1000

Analysis: Goods returned by Bijay or Return Inward A/c is a Nominal A/c. It is a loss – Debit

Return Inward A/c

Bijay is a Personal A/c, here Bijay is the giver – Credit Bijay A/c

Journal Entry:

Note: L/F or Ledger Folio is folio/page number in Ledger linked with Journal entries.

Example 9:

Transaction: Discount allowed ₹ 500

Analysis: Discount is a Nominal A/c, discount allowed is an expense – Debit discount A/c

Cash A/c is a Real A/c – cash going out – Credit Cash A/c

Journal Entry:

Example 10:

Transaction: Interest received ₹1000 from Bank

Analysis: Interest is a Nominal A/c – Interest received is an income – Credit Interest A/c Bank is Real A/c Amount coming in – Debit Bank A/c

Journal Entry:

Subsidiary Books or Sub-Journal:

We have learnt that all business transactions are recorded for the first time in Journal which is called the Book of original entry. With the expansion of business, the process of recording huge number of transactions in a single journal book became cumbersome and time consuming. To remedy this, the journal was divided into a number of special or subsidiary journals for quick and efficient recording of transactions, each of which would record a specific type of transaction. The criteria of the division were similarity of transactions. For example, all cash transactions were grouped under one book, all credit sales transactions were recorded in another book, and all credit purchase transactions in yet another book, and so on. Special journals proved economical as manpower could be used more efficiently. Some transactions, because of their non-similar nature could not be recorded in any special journal, so they were entered in another subsidiary book called the Journal Proper. The following are the special purpose journals also called subsidiary books:

| 1. Cash Book | For recording Cash and Bank transactions |

| 2. Sales Book | For recording credit Sales |

| 3. Purchase Book: | For recording credit Purchases |

| 4. Purchase Return Book: | For goods returned to seller (Return Outward Book) |

| 5. Sales Return Book: | For recording goods returned by buyer (Return Inward Book) |

| 6. Bills Receivable Book | This records receipt of Bills of Exchange, Hundies etc from parties |

| 7. Bills Payable Book | For recording issue of Bills of Exchange, Promissory notes etc to parties |

| 8. Journal Proper: | Journal proper records transactions which do not fall in any of the above Categories. These are Opening entries, Closing Entries, Adjustment Entries, Rectification Entries, Transfer Entries, Miscellaneous Entries. |

Subsidiary Books – Importance:

1. Easy Reference: Subsidiary books are specialised books that provide easy reference

points for transactions. This is particularly important for credit Sales and Purchase.

2. Increased efficiency: Transaction specific record in separate daybooks is a kind of division of labour which help increase efficiency. This speeds up accounting process.

3. Better Cash Management: In any business cash and bank transactions are many and indicate the health of the concern. Monitoring cash becomes easier through the subsidiary Cash Book. Errors and frauds can thus be prevented.

4. Flexibility: A business organisation can subdivide a specific day book and manage the accounts more efficiently. For example, Sales Day Book may be subdivided into area wise Sales Books for better control over sales.

5. Convenience in Audit: Subsidiary books make an Auditor’s job easier. They can locate and check transactions easily without having to rummage through whole lot of transactions.

Subsidiary Books – key features:

1. Purchase Book, Sales Book, Purchase Return Book, Sales Return Book, Bills Receivable Book, Bills Payable Book – all record credit transactions.

2. Transactions in the above Subsidiary Books are written in Statement format. In other words, these are records of credit transaction and not accounting entries.

3. Not being individual accounts balancing is not done. Only, recorded amounts of Purchase, Sales, Return Outward and Return Inwards are summed up periodically and transferred to respective ledger accounts where ultimately balancing is done. For example, the total of the Purchase Book is transferred to Purchase Account.

4. Being Statements and not accounts, the Purchase/Sales/Bills Receivable/Bills Payable Book totals are not transferred to Trial Balance.

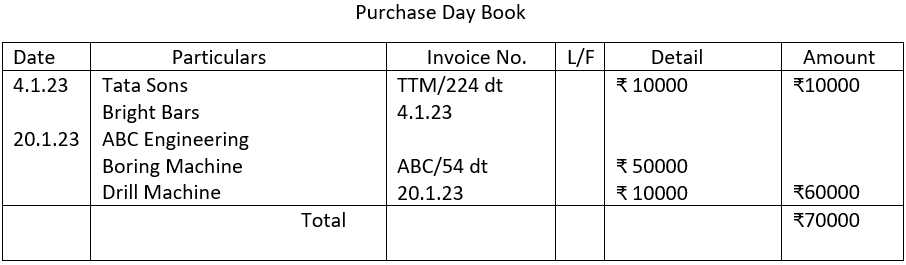

Purchase (Journal) Book:

All credit purchases of goods are recorded in the purchase journal whereas all cash purchases are recorded in the Cash Book. The basis of the journal entry will be bills, invoices etc. Other purchases such as purchase of office furniture, equipment, building, machinery are recorded in the journal proper if purchased on credit or in the cash book if purchased for cash. Monthly total of the purchase book is posted on the debit side of the purchase account in the ledger about which we will discuss later.

Illustration of Purchase Day book

Transaction 1. Purchased steel bars worth ₹20000 on credit from Tata Sons

Source: Invoice no. TTM/224 dt. 4.1.23

Transaction 2. Purchased on credit Machinery valued ₹50000 and one drill machine for ₹10000

from ABC Engineering

Source: Invoice No. ABC/54 dt. 20.1.23

Note: The total amount of ₹70000 will be transferred to Purchase Account in the ledger.

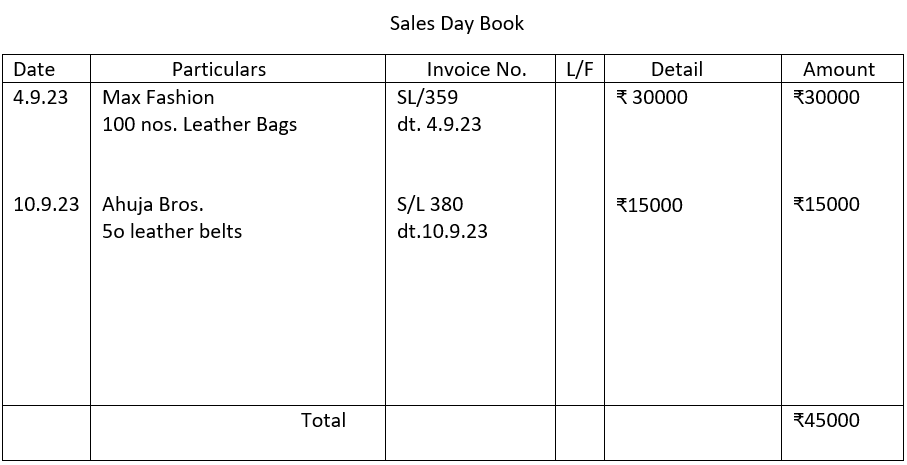

Sales (journal) Book:

All credit sales of merchandise are recorded in the sales day book. Cash sales are recorded in the cash book. The source documents for recording entries in the sales journal are sales invoice or bills issued by the firm to customers. Periodically the sales book is totalled and posted in sales account in the ledger. Sale of assets of a company is not recorded in the sales journal. Illustration:

Transaction 1. Sold 100 nos. of leather bags at a price of ₹30000 on credit to Max Fashion

Source: Invoice no. SL/359 dt 4.9.23

Transaction 2. Sony & Co. sold 50 nos. leather belts to Ahuja Bros. for ₹ 15000 on credit

Source: Invoice no. SL/380 dt. 10.9.23

Note: The total amount of ₹45000 will be transferred to Sales Account in the Ledger.

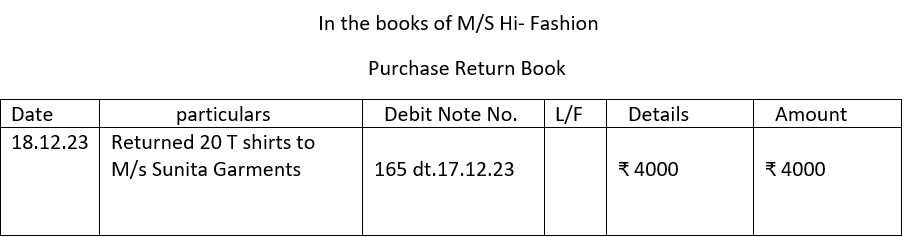

Purchase Return Book:

Sometimes goods purchased by a company or part thereof is returned to the supplier if they have not met the quality standard or are defective. These transactions are recorded in the purchase return journal. For every such return a debit note is prepared and the original copy is sent to the supplier. The debit note is the source document for recording the transaction in the purchase return book. The Individual supplier’s account will be debited with the amount of returned goods. Periodically, the amount column of the purchase return book is totalled and posted to the credit side of the purchase account in the ledger.

Illustration:

Transaction: M/S Hi-Fashion Returned 20 T-shirts valued at ₹4000 to M/ Sunita garments for poor quality

Source document: Copy of Debit note no 165 dt 17.12 23 sent to M/s Sunita Garments

Note 1. Refer to illustration of Debit Note given earlier

2. Total of Purchase Return Book will be transferred to Return Outward book in ledger

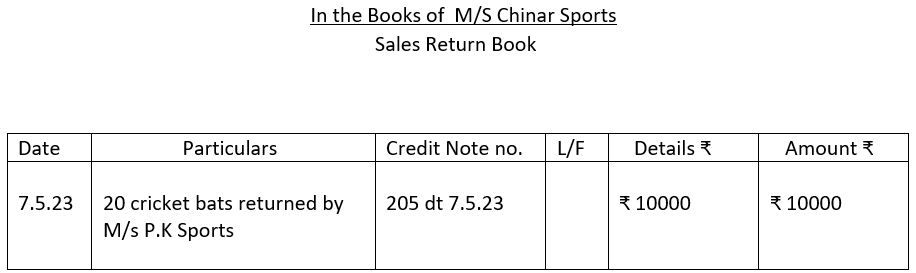

Sales Return Book:

This journal is used to record value of items returned by a customer for quality issues. On receipt of the of goods from customer, a credit note is prepared by the seller giving detail of the goods returned and the value thereof. This is the source material used to record the transaction in the Sales Return journal and the customer account is credited in the ledger.

Illustration:

Transaction : M/S PK Sports returned 20 cricket bats bought on credit from M/S Chinar Sports and valued at ₹ 10000

Source document : Credit note no.205 dt 7.5.23

Note 1. Refer to illustration of credit note given earlier

Note 2. Total of Sales Return Book will be transferred to Return Inward A/C in ledger

Journal Proper:

There are certain important transactions which cannot be accommodated in special journals mentioned above. A separate book known as Journal Proper is maintained to record them. The entries recorded in Journal Proper are as follows:

Opening Entries:

At the beginning of a new financial year new set of books are opened with opening balances of assets, liabilities and capital. These opening entries are recorded in Journal Proper.

Adjustment Entries:

In order to upgrade ledger account on accrual basis such entries are made at the end of accounting period. Such as Rent Outstanding, Prepaid Insurance, depreciation and Commission received in advance etc.

Rectification Entries:

Rectification Journal Entries are passed to rectify errors in recording transactions in journal and posting to ledger. These are done in Journal Proper.

Transfer Entries / Closing Entries:

Accounts relating to operation of business such as Sales, Purchases, Opening stock, Incomes, Gains and Expenses, etc. and drawing are closed at the end of the year and their Total/balances are transferred to Trading and Profit & loss account by recording the journal entries. These are also called closing entries.

Other Entries

1. Cancellation of discount in case of dishonour of a cheque

2. Goods withdrawn by owner for personal use

3.Endorsement and dishonour of Bills of exchange

4. Goods distributed as free sample

5. Loss of goods by fire, theft or pilferage

Examples of Journal Entries from transactions:

Journal entries in the books of Dilip & Co.

CBSE Class 9 Elements of Book-Keeping and Accountancy Unit 4: Journal – Completed

We have completed the following topics in this unit:

Content:

Need for journal and journal entries

Subsidiary Books – Cash Book, Purchase Book, Sales book, Purchase Return Book, Sales Return Book

and Journal Proper

Learning Outcomes:

Understanding the need for journal

Developing the skill of recording of transactions in journal

Explaining the importance of preparing subsidiary books